November 4, 2022

When considering risks, Sherlock first evaluates the downside, by Howard Rankin

Computers Learn from Human Strategies to Comprehend Human Markets, by Michael Hentschel

Our computers found the optimum ratio between risk and gain, by Grant Renier

When considering risks, Sherlock first evaluates the downside

“Is it worth going to interview that woman about the Baskerville murders? I suspect she knows very little if anything of relevance,” Watson asked.

“Not sure. I’m still weighing it in my mind,” said Sherlock. “Maybe tomorrow could be better spent revisiting the scene of the crime. But who knows? Perhaps she has the one piece of information that is critical to the investigation.”

“You have said on many occasions that timing is critical. I’m just concerned we would be wasting valuable time we can’t get back,” said Watson. “It just feels wrong.”

“There’s no information that can guide us here,” said Holmes. “We have to take a risk, whatever we choose.”

“Well, is there any way we can mitigate the risk, Holmes?” asked Watson.

“Good point. We could hedge our bets, so to speak. First thing, tomorrow, Watson, you head down to meet with the lady, and I’ll go straight to the scene of the crime. Then you can meet me there when you’re done.”

“I appreciate your trust in me Sherlock. May I ask you in which school did you learn such wisdom?”

“Elementary, my dear Watson.”

When considering risks, we typically first evaluate the downside. What’s the worst that could happen? If that cost is bearable, then how should we proceed? This is the initial fast and frugal thinking analysis, which might then be influenced by sensations, arising from the gut, the subconscious, or anywhere else within our mind-body.

The sensations we feel influence the thoughts we have. How much and in what way they do this are the core issues around which IntualityAI operates. The evaluation of risk can be so circumstantial and individualized but nevertheless there is decent empirical support for the notion that, as a general rule, a 2.5:1 ratio is the tipping point. If the probability of a reward is less than 2.5:1 i.e., for a ten dollar wager you wouldn’t make any more than $25, most people are not interested. As the possible reward exceeds this ratio, the risk seems to be warranted by the possibility of a bigger pay out.

Specifically, we can get a sense of anxiety, as we face any decision. That anxiety could be anything from a mild sense of uneasiness to a full-blown panic attack. That feeling of tension is influenced by many variables, such as time of day, the social environment, and even how much you had to drink the night before. However, hedging allows us to modify the risks and payoffs. In such ways are decisions made about future possibilities.

by Howard Rankin PhD, psychology and cognitive neuroscience

Hedging Investment Risk and Gain – Computers Learn from Human Strategies to Comprehend Human Markets

My own highly risky private venture investments in the past earned an average 28% IRR over ten years, which was considered extraordinary at the time, and only 3 of the companies accounted for most of that gain, while the other 7 became “living-dead” drags on superior performance. This involved considerably more risk than standard equity markets, with considerably greater rewards, possible but by no means assured.

And while my VC team and I chose from at least 3000 Business Plans over time, even the best venture investments were highly illiquid and mysterious. Once you got in, it was exceedingly hard to get out.

Hedging was achieved by pitting high-risk companies against even

higher-risk companies, a creatively human portfolio strategy. Rational? Irrational? Both?

In public equity portfolio investment performance, a central attraction of any previous simulated and tested Fund will always be its ability to hedge the losses as markets and companies tank, while still outperforming other methods of portfolio management when markets gain. This must look at many more actual investments, and much more trading.

Computers need to assist, or more correctly stated, humans must assist the computers processing the enormous data continually generated just to trade equities or futures. How even to measure risk in such an environment? How then to manage the risk-gain volatility? The best of both worlds, of risk-taking and hedge analytics, is called for at every instant. Human-designed computers must work seamlessly in a human-caused market environment.

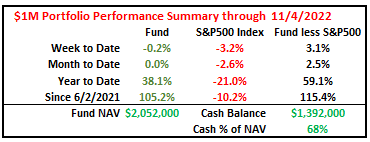

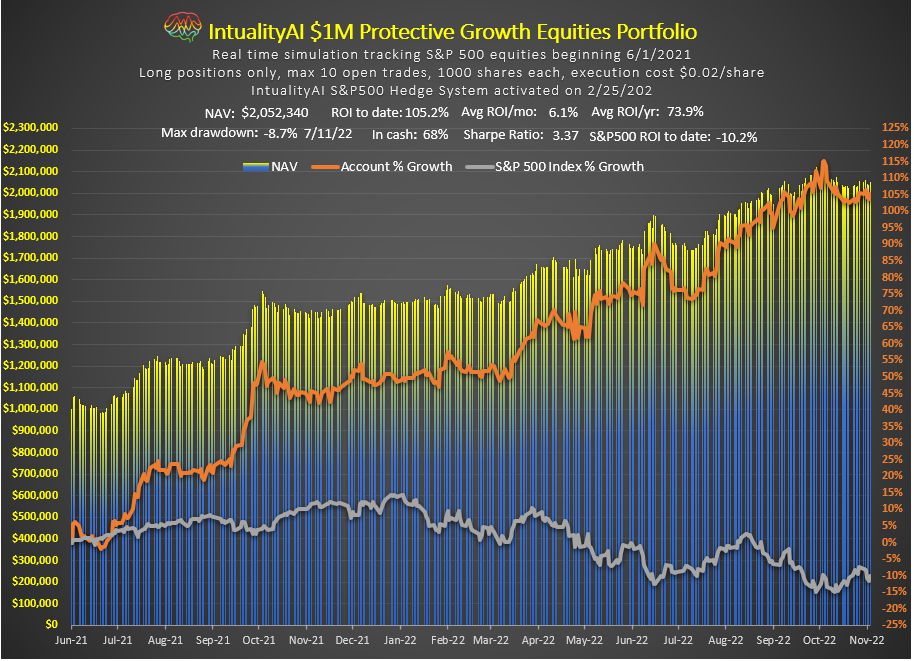

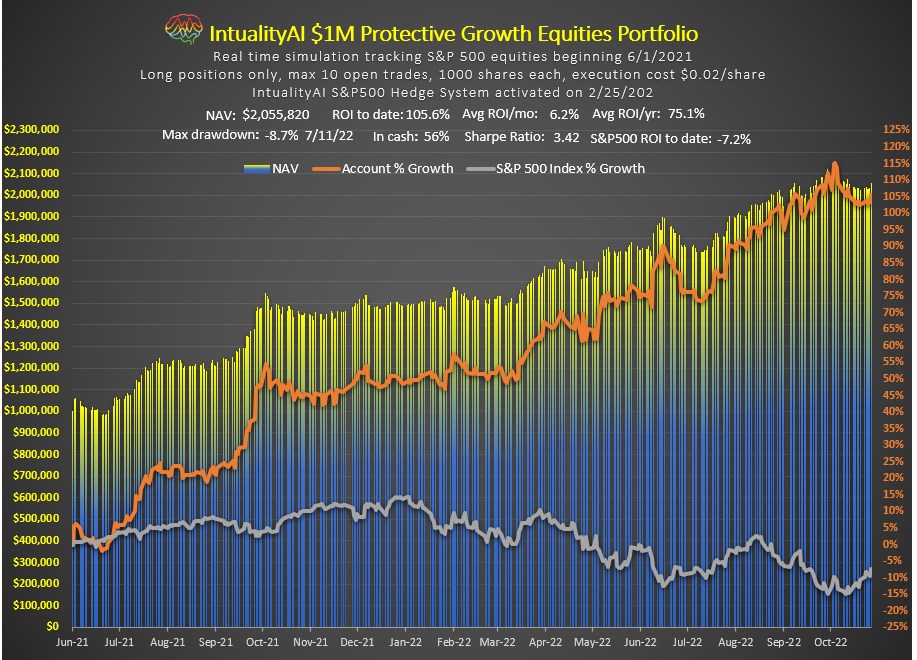

Our upcoming $1 million S&P500 Fund is expected to debut this month. It will be our first true big-money implementation, and that size of Fund in simulation over the past 18 months has been nothing short of amazing: Averaging 6% gains each of the 18 months has achieved 18-month 122% ROI and annualized 75% ROI so far, with very few downcycles, beating the S&P500 110% to 5%.

As they say (and as we must say), past results do not prove or provide future results. We don’t know if the newest Fund will do nearly as well as the models, but there is no reason it cannot repeat its modeled algorithmic “Protective Growth” characteristics of the past: hedging combined with aggressive growth objectives.

So how does IntualityAI hedge? The AI’s comprehensive analysis of ALL portfolio choices each and every day and every micro-second cannot be replicated by any human-alone, nor especially the picking mechanism based on all the observed trend biases, nor the individual-trade avoidance or change-of-holding of specific trades.

Every Human has a personal risk-reward profile and comfort zone. In my own present “simplified” personal portfolio strategy favoring Tesla, for example, I have been dismayed but not surprised nor disappointed to note that IntualityAI has generally avoided even getting close to taking a Tesla position as I personally manage, and yet has outperformed me with much less promising equity choices. This is because my personal risk profile looks much farther into the future than most market participants, who get perturbed by near-term events that create enormous volatility, which I only see as buying opportunities to get myself even deeper into this risk. The last thing I want personally is risk-avoidance, though I have “interim” losses on quite a few of my Tesla purchases. I would have done better skipping those losses.

IntualityAI’s “interim thinking” can be tracked and used for prediction and ideas, individually and in portfolios. We can know when IntualityAI is getting close to making buy or sell decisions on any S&P500 stock the program currently tracks historically and in real time. And Intuality’s real computer-enhanced genius applies especially well to managing a complete portfolio of stocks or futures, for risk, hedging, and maximum reward.

by Michael Hentschel, Yale and Kellogg anthropology, economics, venture capital

Our computers found the optimum ratio between risk and gain

Research shows that given a chance to win $100 or avoid losing $100, most people choose not to lose money rather than speculate. However, as the benefits of the potential gain rise, choices change. More people would choose to risk losing $100 if the prize was $1000. Many more would risk losing $100 if the prize was $10,000. And each week many people are prepared to risk around $20 for a chance to win billions in the lottery, even though the chance of winning is minute but hey, someone’s got to win, right?

Actually, no, there is no guarantee that the major prize is won each week, and in any event, the talk is about the $1.6 billion that someone could win, not the $20 you are almost certain to lose.

The results of extensive research to determine a mathematical relationship between risk and gain were surprising! Heavy computer number crunching showed that the relationship was non-linear between the two extremes, like the real-world examples, above. Not only that, and regardless of the application, the mathematical risk/gain relationship converged on a consistent value within a simple formula.

The value was 2.5:1, the general value of perceived risk over gain, basically confirming how we behave. We are a risk averse specie. When calculating the probabilities of future events as being on either side of 50:50, our humanized AI uses an adjusted probability of 72:28 in

favor of risk. The variables were found to be direct functions of the size of the potential risk versus gain relationships, independent of the application sectors.

When confronted with potential risk versus gain, human behavior and resulting decisions were showing high degrees of consistency for all applications, regardless of their apparent disconnectedness. And our computers found this to be the optimum ratio regardless of the application: like bets on football games, trading in the markets, predicting winning politicians and heart arrythmias, and even the direction of random number series.

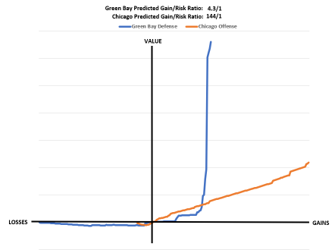

The chart above shows the 69th play of the game between the Green Bay Packers and the Chicago Bears with Chicago on offense. The humanized AI curve for that play (1 day before the actual game) indicated that Chicago could choose potential gain (go for it) over risk (punt) given the high gain ratio of 144 to 1, compared to Green Bay’s defense ratio of 4.3 to 1. (Remember, games are all about going for the gains by winning). In actual fact, Chicago went for it with a 5-yard pass play an got a 1st down!

Hedging is an integral function in decision making and game playing. It's the potential offset to failure. It changes the 72/28 ratio towards 50/50, increasing the prospect for gain. And, it can also attempt to eliminate all risk and gain. Chicago could have punted! The S&P 500 Futures Index is typically used to protect stock equity portfolios. But, hedging is never perfect. Some gain or loss always leaks through. Humanized AI knows this and can help by simulating us out of an unhappy future.

by Grant Renier, engineering, mathematics, behavioral science, economics

This content is not for publication

©Intuality Inc 2022-2024 ALL RIGHTS RESERVED